#Short Answer

Covers facts about ai in finance, including core concepts, practical examples, benefits, limitations, and risks in Business & Marketing.

#Infobox

#Overview

Artificial Intelligence (AI) has revolutionized the financial sector by introducing automation, predictive analytics, and data-driven decision-making. AI systems analyze vast datasets to identify patterns, predict market trends, and mitigate risks, enabling financial institutions to operate more efficiently and competitively. From algorithmic trading to personalized banking, AI applications span nearly every facet of finance, reshaping how businesses and consumers interact with financial services. The integration of AI in finance is driven by the exponential growth of big data, advancements in computing power, and the increasing demand for real-time analytics. Unlike traditional rule-based systems, AI models—particularly those leveraging deep learning—can process unstructured data, such as news articles or social media sentiment, to generate actionable insights. This capability has led to the development of sophisticated tools like robo-advisors, which provide automated investment recommendations, and AI-powered fraud detection systems that identify anomalies in transaction patterns. Moreover, AI enhances customer experiences through chatbots and virtual assistants, offering 24/7 support and personalized financial advice. In risk management, AI models assess creditworthiness, predict loan defaults, and optimize portfolio allocations, reducing human error and bias. As AI continues to evolve, its role in finance is expected to expand, with emerging technologies like generative AI and quantum computing poised to introduce further innovations.

#History / Background

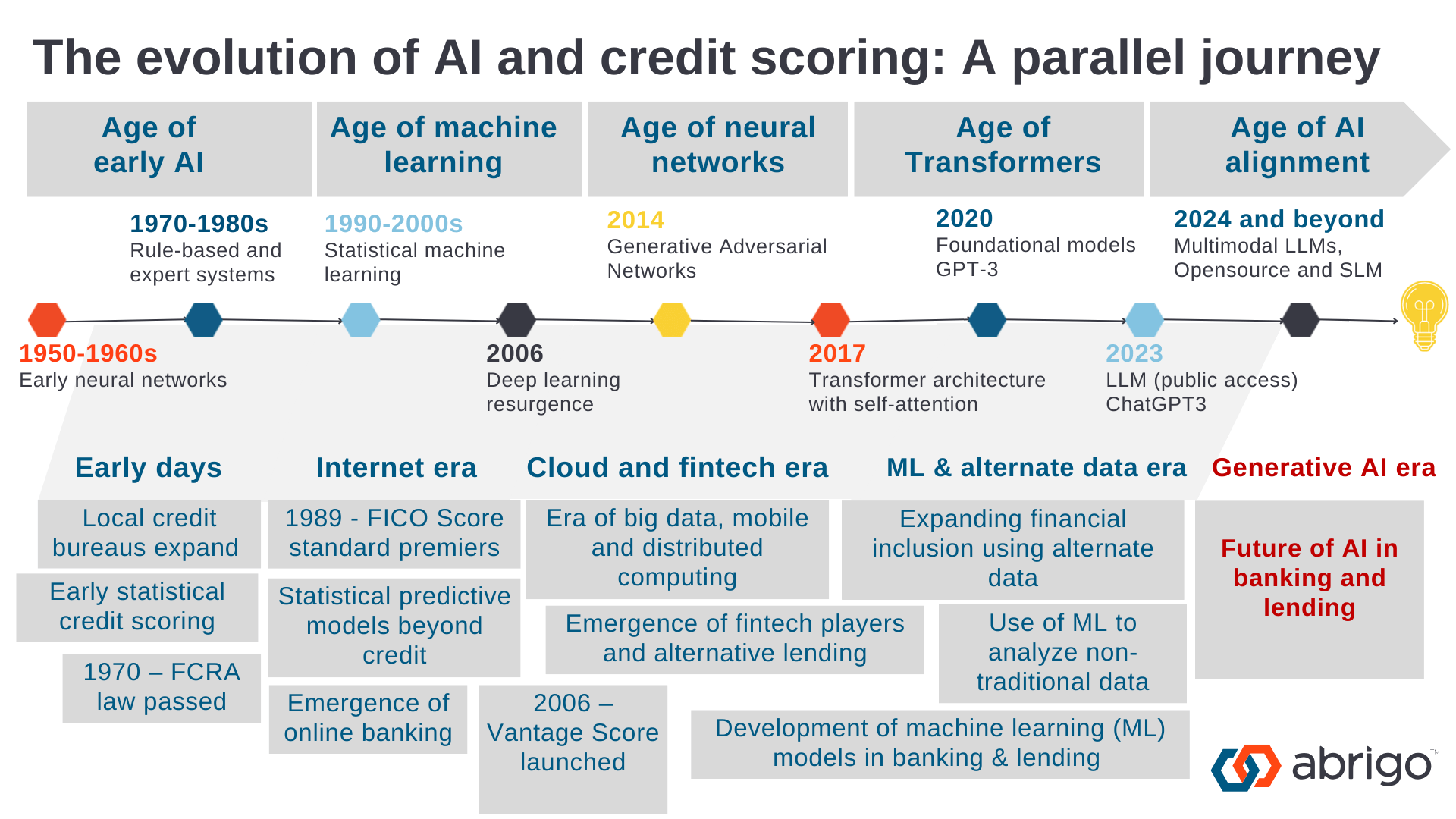

The application of AI in finance traces back to the 1980s, when early expert systems were developed to automate financial decision-making. One of the first notable examples was Prospector, an AI program designed to assist geologists in mineral exploration, which later inspired financial applications. By the late 1980s, banks began experimenting with AI for credit scoring and loan approvals, leveraging rule-based systems to evaluate borrower risk. The 1990s marked a significant shift with the advent of machine learning (ML) algorithms. Financial institutions started using neural networks to predict stock market trends and detect fraudulent transactions. Fidelity Investments and Goldman Sachs were among the pioneers in adopting AI for trading strategies, while JPMorgan Chase developed early AI-driven risk assessment models. The 2000s saw a surge in AI adoption, fueled by the rise of big data and cloud computing. The financial crisis of 2008 accelerated the need for robust risk management tools, prompting banks to invest heavily in AI-driven analytics. BlackRock, the world’s largest asset manager, launched Aladdin, an AI-powered platform for portfolio management and risk analysis. Simultaneously, fintech startups emerged, offering AI-driven solutions for peer-to-peer lending, micro-investing, and automated financial planning. The 2010s witnessed the integration of deep learning and natural language processing (NLP) into financial services. Companies like Ant Group (formerly Ant Financial) and Revolut utilized AI to enhance customer interactions, while hedge funds like Renaissance Technologies and Two Sigma achieved superior returns through AI-driven trading algorithms. The proliferation of smartphones and mobile banking further accelerated AI adoption, enabling real-time financial insights and personalized services. Today, AI in finance is a multi-billion-dollar industry, with applications ranging from algorithmic trading to regulatory compliance. The COVID-19 pandemic further underscored the importance of AI, as financial institutions relied on automation to maintain operations during lockdowns. Regulatory bodies, including the U.S. Securities and Exchange Commission (SEC) and the European Securities and Markets Authority (ESMA), have begun scrutinizing AI’s ethical and systemic risks, ensuring transparency and accountability in its deployment.

#How It Works

AI in finance operates through a combination of machine learning (ML), deep learning, natural language processing (NLP), and robotic process automation (RPA). These technologies enable financial institutions to process vast amounts of data, identify patterns, and make data-driven decisions. Below are the key mechanisms through which AI functions in finance:

#1. Machine Learning (ML) and Deep Learning Machine learning algorithms, particularly supervised learning, unsupervised learning, and reinforcement learning, are foundational to AI in finance. These models are trained on historical data to predict outcomes such as stock prices, credit defaults, or fraudulent transactions.

- Supervised Learning: Used for tasks like credit scoring and fraud detection, where the model is trained on labeled data (e.g., past loan defaults or transaction histories).

- Unsupervised Learning: Applied in customer segmentation and anomaly detection, where the model identifies hidden patterns without predefined labels.

- Reinforcement Learning: Utilized in algorithmic trading, where AI agents learn optimal strategies by interacting with market environments and receiving feedback. Deep learning, a subset of ML, employs neural networks with multiple layers to process complex datasets. Convolutional Neural Networks (CNNs) analyze financial time-series data, while Recurrent Neural Networks (RNNs) and Long Short-Term Memory (LSTM) networks predict stock market trends and exchange rates.

#2. Natural Language Processing (NLP) NLP enables AI systems to interpret and generate human language, facilitating applications such as:

- Sentiment Analysis: Evaluating news articles, social media posts, and earnings calls to gauge market sentiment and predict asset price movements.

- Chatbots and Virtual Assistants: Providing customer support, answering queries, and offering financial advice (e.g., Bank of America’s Erica or HSBC’s Amy).

- Document Processing: Automating the extraction of key information from financial reports, contracts, and regulatory filings.

#3. Robotic Process Automation (RPA) RPA uses AI-powered software bots to automate repetitive tasks such as:

- Data Entry: Processing loan applications, updating customer records, and reconciling accounts.

- Compliance Checks: Ensuring adherence to regulatory requirements (e.g., Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols).

- Report Generation: Creating financial statements and audit reports with minimal human intervention.

#4. Computer Vision AI-powered computer vision is employed in:

- Check Processing: Automatically reading and verifying handwritten or printed checks.

- Fraud Detection: Analyzing transaction receipts and identifying forged documents.

- Asset Management: Monitoring physical assets (e.g., real estate, inventory) via drone or satellite imagery.

#5. Predictive Analytics AI models leverage historical and real-time data to forecast:

- Market Trends: Predicting stock price movements, commodity prices, and currency fluctuations.

- Credit Risk: Assessing borrower default probabilities using alternative data sources (e.g., social media activity, utility payments).

- Fraud Patterns: Detecting unusual transaction behaviors in real time.

#6. Blockchain and AI Integration AI enhances blockchain applications in finance by:

- Smart Contracts: Automating contract execution based on predefined conditions.

- Cryptocurrency Trading: Using AI to analyze market trends and execute trades in decentralized finance (DeFi) platforms.

- Fraud Prevention: Identifying suspicious transactions on blockchain networks.

#Important Facts

#1. AI in Algorithmic Trading - AI-driven trading algorithms account for over 70% of U.S. stock market trading volume (as of 2023). - Hedge funds using AI, such as Renaissance Technologies and Two Sigma, consistently outperform traditional funds, with some achieving annual returns exceeding 20%. - AI models can execute trades in milliseconds, far faster than human traders, reducing latency and improving profitability.

#2. Fraud Detection and Prevention - Financial institutions lose $5.1 trillion annually to fraud, but AI reduces losses by up to 50% through real-time transaction monitoring.

- Mastercard’s Decision Intelligence uses AI to analyze 160 billion transactions per year, flagging fraudulent activities with 95% accuracy.

- Deep learning models can detect synthetic identity fraud, where criminals create fake personas using stolen or fabricated data.

#3. Credit Scoring and Lending - Traditional credit scoring (e.g., FICO) relies on limited data, excluding 60% of the global population from formal credit. - AI models incorporate alternative data (e.g., mobile phone usage, social media activity, rental payments) to assess creditworthiness, expanding access to loans for underbanked populations.

- ZestFinance and Upstart use AI to approve loans for borrowers with thin credit files, reducing default rates by 30-50%.

#4. Robo-Advisors and Wealth Management - The global robo-advisory market is projected to reach $1.5 trillion by 2025, growing at a CAGR of 25%. - Platforms like Betterment and Wealthfront use AI to optimize investment portfolios, reducing fees by 0.25-0.5% compared to traditional advisors. - AI-driven robo-advisors can rebalance portfolios automatically based on market conditions and investor risk tolerance.

#5. Customer Service and Personalization

- 80% of banking customers prefer AI-powered chatbots for quick queries, reducing wait times by up to 90%.

- JPMorgan’s COIN (Contract Intelligence) reviews 12,000 commercial loan agreements per second, saving 360,000 hours of work annually. - AI personalizes financial products by analyzing spending habits, investment goals, and life events, increasing customer retention by 20-30%.

#6. Regulatory Compliance and Risk Management - AI helps banks comply with AML (Anti-Money Laundering) and KYC (Know Your Customer) regulations by automating suspicious activity reporting.

- HSBC’s AI system processes 5 billion transactions daily, identifying potential money laundering with 99% accuracy. - Regulatory bodies like the SEC and ESMA are developing AI-specific guidelines to address biases, explainability, and systemic risks.

#7. Challenges and Limitations

- Bias in AI Models: Algorithms trained on historical data may perpetuate discrimination in lending (e.g., racial or gender bias in credit scoring).

- Explainability: Complex AI models (e.g., deep learning) are often "black boxes," making it difficult to justify decisions to regulators or customers.

- Cybersecurity Risks: AI systems are vulnerable to adversarial attacks, where hackers manipulate input data to deceive models (e.g., spoofing fraud detection systems).

- Data Privacy Concerns: Financial institutions must comply with GDPR, CCPA, and other regulations while using customer data for AI training.

#Timeline

- Foundational ideas

Core concepts and early methods shape Facts About AI in Finance.

- Practical use

Tools, examples, and real-world deployments make the topic easier to evaluate.

- Responsible implementation

Current work focuses on reliability, governance, performance, and measurable impact.

#Related Terms

#FAQ

What does Facts About AI in Finance cover?

Covers facts about ai in finance, including core concepts, practical examples, benefits, limitations, and risks in Business & Marketing.

Why is Facts About AI in Finance important?

It helps readers understand key concepts, compare practical use cases, and evaluate how Business & Marketing decisions affect outcomes, risks, and implementation choices.

What should readers verify before applying this topic?

Readers should compare benefits, limitations, data requirements, and related themes such as Facts, About, AI before using the ideas in real projects.

#References

- Facts About AI in Finance terminology and background research

- Facts About AI in Finance use cases, implementation examples, and limitations

- Business & Marketing best practices, standards, and risk guidance

- Facts case studies, benchmarks, and current industry analysis

Comments

No comments yet. Start the discussion with a useful note.