#Short Answer

Compares AI in finance with traditional banking, clarifying differences, strengths, limitations, and practical use cases.

#Infobox

AI in Finance vs Traditional Banking Field Finance Focus Automation, Decision-Making, Customer Experience Key Technologies Machine Learning, Natural Language Processing, Predictive Analytics Primary Users Banks, Fintech Companies, Investors, Consumers Adoption Rate Rapidly Increasing (2020s) Regulatory Status Evolving (AI-specific regulations emerging)

#Overview

AI in finance represents a paradigm shift from conventional banking methods by incorporating advanced computational techniques to analyze vast datasets, detect patterns, and make real-time decisions. Traditional banking, rooted in centuries-old practices, operates through structured workflows, manual verification, and centralized control. The convergence of AI and finance has given rise to fintech innovations, including robo-advisors, algorithmic trading, fraud detection systems, and AI-powered chatbots. These technologies aim to enhance accuracy, reduce human error, and deliver personalized financial services at scale.

In contrast, traditional banking institutions emphasize regulatory compliance, risk management through human oversight, and customer service based on interpersonal trust. While both models coexist, AI-driven finance is rapidly gaining traction due to its ability to process large volumes of data and adapt to dynamic market conditions. However, challenges such as data privacy, algorithmic bias, and cybersecurity risks remain critical considerations in the adoption of AI within financial ecosystems.

#Key Differences

- Decision-Making: AI systems rely on data-driven algorithms, whereas traditional banking depends on human judgment and established policies.

- Speed and Efficiency: AI enables real-time processing and automation, reducing operational delays common in manual banking systems.

- Personalization: AI tailors financial products to individual needs using behavioral data, while traditional banking often offers standardized services.

- Scalability: AI solutions can be deployed globally with minimal incremental costs, unlike traditional banking, which requires physical infrastructure and staffing.

- Regulatory Adaptability: Traditional banks operate under well-defined regulatory frameworks, while AI in finance is navigating emerging regulations specific to algorithmic decision-making.

#History / Background

The evolution of AI in finance can be traced back to the 1980s and 1990s, when early applications of expert systems and statistical models were used for credit scoring and risk assessment. The development of machine learning algorithms in the 2000s, particularly with the rise of big data, accelerated AI adoption in financial services. The 2010s saw the emergence of fintech startups that leveraged AI to disrupt traditional banking models, offering peer-to-peer lending, automated investment platforms, and AI-driven customer service.

Traditional banking, with its origins in ancient Mesopotamia and the Renaissance banking systems of Italy, has evolved through industrialization and digital transformation. The introduction of ATMs in the 1960s and online banking in the 1990s marked early steps toward modernization. However, the core principles of traditional banking—trust, stability, and regulatory oversight—remain unchanged. The financial crisis of 2008 further highlighted the need for innovation, prompting traditional banks to explore AI solutions to enhance resilience and customer engagement.

#How It Works

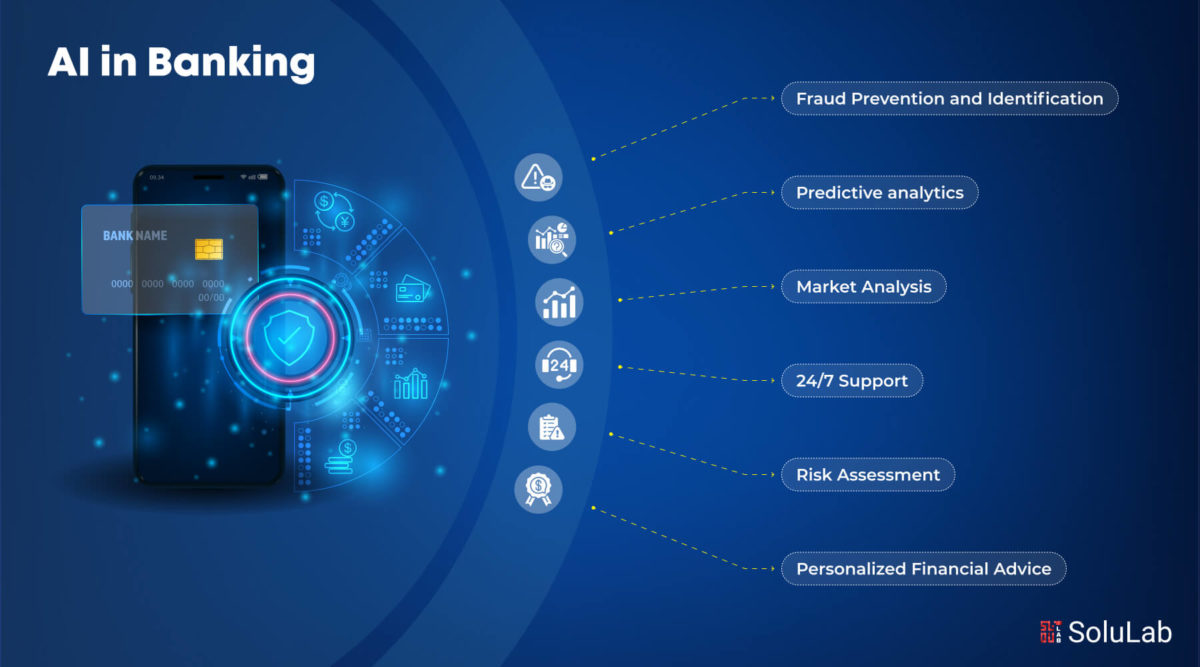

#AI in Finance

AI in finance operates through several core technologies:

- Machine Learning (ML): Algorithms analyze historical and real-time data to identify trends, predict market movements, and optimize trading strategies. Supervised learning is commonly used for credit scoring, while unsupervised learning helps detect anomalies in transaction patterns.

- Natural Language Processing (NLP): Enables systems to interpret human language, facilitating chatbots, sentiment analysis, and automated document processing. NLP powers virtual assistants that handle customer inquiries and extract insights from earnings calls or financial reports.

- Predictive Analytics: Uses statistical models and ML to forecast financial outcomes, such as loan defaults, stock prices, or customer churn. This helps institutions mitigate risks and tailor product offerings.

- Computer Vision: Analyzes visual data from documents, receipts, or surveillance footage to automate processes like check processing or fraud detection.

- Reinforcement Learning: Optimizes decision-making in dynamic environments, such as algorithmic trading, where systems learn from outcomes to improve future actions.

#Traditional Banking

Traditional banking relies on a combination of manual processes, standardized procedures, and human oversight:

- Branch Operations: Customers interact with tellers and advisors for services such as deposits, loans, and account management. Physical branches remain a cornerstone of customer trust and relationship-building.

- Credit Assessment: Loan approvals are determined through standardized criteria, including credit scores, income verification, and collateral evaluation. Human underwriters review applications to assess risk.

- Risk Management: Banks employ teams of risk analysts to monitor portfolios, comply with regulations, and implement controls to prevent fraud or financial instability.

- Transaction Processing: Clearing and settlement of payments are handled through centralized systems, often involving intermediaries like SWIFT or ACH networks.

- Customer Service: Support is provided via call centers, in-person consultations, and written correspondence, emphasizing personalized relationships.

#Important Facts

- Adoption Growth: According to a 2023 report by McKinsey, AI adoption in financial services has increased by over 60% since 2018, with banks investing $20 billion annually in AI-related technologies.

- Fraud Detection: AI systems can identify fraudulent transactions with up to 95% accuracy, compared to 70-80% accuracy in traditional rule-based systems.

- Cost Efficiency: AI-driven automation can reduce operational costs in banking by up to 30%, primarily through reduced staffing and error correction.

- Regulatory Challenges: The European Union’s GDPR and the EU AI Act impose strict guidelines on AI usage in finance, particularly regarding data privacy and algorithmic transparency.

- Customer Expectations: A 2024 survey by Deloitte found that 72% of consumers prefer AI-powered financial services for speed and convenience, while 58% still trust traditional banks for security and reliability.

- Job Displacement: The World Economic Forum estimates that AI and automation could displace 85 million jobs globally by 2025, with 40% of banking tasks being automatable.

#Timeline

Year Event 1980s Introduction of expert systems for credit scoring and risk assessment in banking. 1997 IBM’s Deep Blue defeats world chess champion Garry Kasparov, demonstrating AI’s potential in complex decision-making. 2006 Launch of peer-to-peer lending platforms like Prosper and LendingClub, leveraging data-driven lending models. 2011 IBM Watson wins Jeopardy!, showcasing AI’s ability to process natural language and make data-driven decisions. 2014 Apple Pay and Google Wallet introduce mobile payment systems, integrating AI for fraud detection and user authentication. 2016 AlphaGo, developed by DeepMind, defeats a professional Go player, highlighting advancements in deep learning. 2018 European Union introduces the GDPR, setting global standards for data privacy in AI applications. 2020 COVID-19 pandemic accelerates digital banking adoption, with AI-powered chatbots handling 80% of customer inquiries in some institutions. 2022 Launch of generative AI models like ChatGPT, enabling advanced financial advisory and automated report generation. 2023 U.S. Federal Reserve and European Central Bank begin pilot programs for AI-driven monetary policy analysis. 2024 Global fintech investments exceed $200 billion, with AI startups comprising 35% of the total.

#Related Terms

#FAQ

What does AI In Finance Vs Traditional Banking: What’s The Difference? cover?

Compares AI in finance with traditional banking, clarifying differences, strengths, limitations, and practical use cases.

Why is AI In Finance Vs Traditional Banking: What’s The Difference? important?

It helps readers understand key concepts, compare practical use cases, and evaluate how Business & Finance decisions affect outcomes, risks, and implementation choices.

What should readers verify before applying this topic?

Readers should compare the benefits, limitations, data requirements, and related themes such as Comparison, Trade Offs, Finance before using the ideas in real projects.

#References

- AI In Finance Vs Traditional Banking: What’s The Difference? terminology and background research

- AI In Finance Vs Traditional Banking: What’s The Difference? use cases, implementation examples, and limitations

- Business & Finance best practices, standards, and risk guidance

- Comparison case studies, benchmarks, and current industry analysis

Comments

No comments yet. Start the discussion with a useful note.